Gone are the days where you can “bank-and-earn” just by crediting your salary and spending on your credit card. As recently as 2019, a total transaction of SGD $5,000 on the above with DBS Multiplier was enough to earn you 1.9% p.a. interest.

Today, that same salary and credit card spend combo will only get you 0.5% p.a. interest. Not fabulous, but at least it’s better than the 0.05% interest you will get on a basic savings account.

And with the US Federal Reserve pledging to keep interest rates near zero for the next 2 – 3 years, it’s unlikely interest rates for the popular high yield savings accounts like DBS Multiplier, OCBC 360 and Standard Chartered JumpStart will go up anytime soon.

Are fixed deposits a good alternative? Well, if you’re fine with your money being locked up anywhere from 12 to 18 months, they do offer slightly better interest than savings accounts. Right now, the highest fixed deposit rate is from DBS at 1.3% p.a. when you deposit a minimum of $1,000 for 18 months.

If you’re looking for alternatives to savings accounts or fixed deposits for your hard-earned money, there are 2 worthwhile options to consider.

#1: Insurance savings plans: We use the term here loosely, but generally these are products that combine savings with a life insurance coverage.

Note: Since new sign-ups for the Singlife Account have been on hold from 15 December 2020, the next best options are SingTel’s Dash EasyEarn Insurance Savings Plan and GIGANTIQ by insurer Etiqa.

#2: Cash management products: These have an investing element. Your money is invested into very low-risk money market funds (MMF) and short-duration bond funds.

Note: At present, only Stashaway, Syfe and Endowus offer projected returns of more than 1.4% p.a. We will be covering these in detail here.

Singtel Dash EasyEarn: What is it?

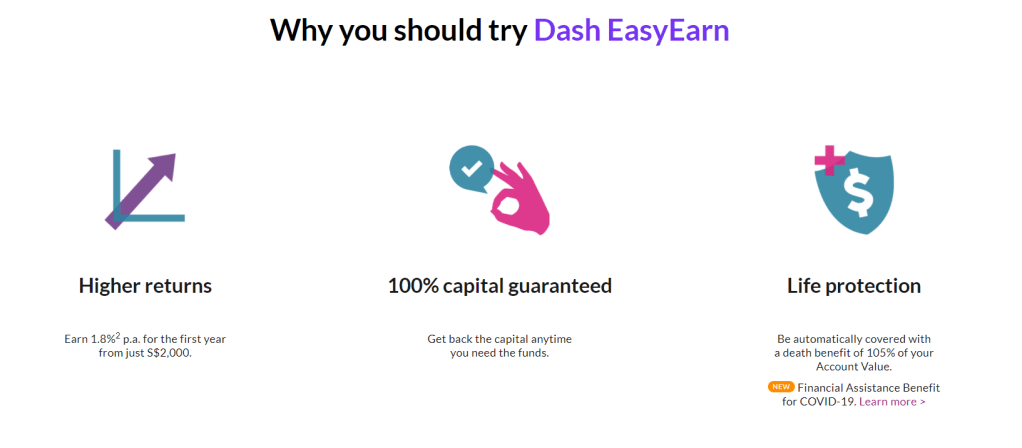

Getting straight to it, Dash EasyEarn offers you a guaranteed return of 1.8% p.a. for the first policy year (a guaranteed 1.5% p.a. and an additional 0.3% p.a. bonus return). The total account value that earns this interest is $2,000 to $20,000. To be eligible for this advertised rate, you need to maintain at least $2,000 average daily account value.

From the second policy year, it is not clear what the rate will be. However, they could still maintain it around 1.5% p.a. depending on the interest rate environment then.

If you have a substantial amount of emergency savings or spare cash, one major disadvantage of Dash EasyEarn is the account value cap of $20,000. In other words, you won’t be able to park more than $20,000 of your savings with Dash EasyEarn.

Singtel Dash EasyEarn: Deposit and withdrawals

You can deposit and withdraw anytime with no lock-ups. The process is very straightforward.

Sign up for Dash EasyEarn via Singtel Dash app (If you’re a new customer, you can use the referral code OBCloem).

Make your first top-up (minimum of $2,000) through the app by transferring funds from your bank account (via eNETs). All future top-ups can be made through the app too. However, they must be made in multiples of $500, so if you’re thinking of topping up $888 for Chinese New Year, that won’t be possible.

To withdraw, you must withdraw in multiples of $100. You can do so anytime for free only if you withdraw directly to your Dash mobile wallet. If you want to withdraw to your bank account, a processing fee of $0.70 applies.

GIGANTIQ: What is it?

GIGANTIQ is offered by Etiqa, a leading insurer that is also part of the Malaysian banking group, Maybank.

GIGANTIQ offers 1.8% p.a. returns on your first $10,000 for one year (guaranteed 1% p.a. and 0.8% p.a. bonus). Amounts above $10,000 will receive 1% p.a. for the first year as well. Beyond that, you will get prevailing market rates for subsequent years with your capital guaranteed.

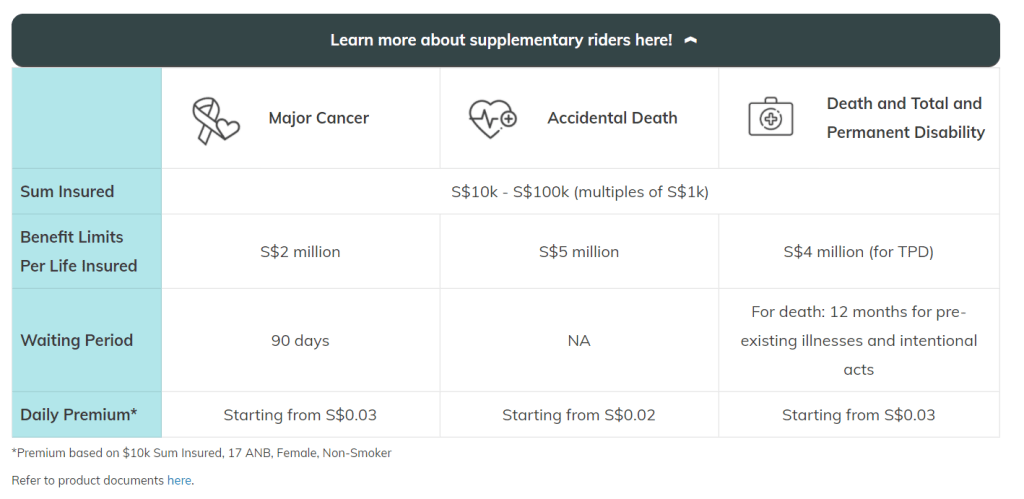

If you want to earn higher interest, you can consider adding on the following supplementary riders to your plan. For every rider purchased, you will earn an extra 0.25% p.a. on your first $10,000 account value. So one GIGANTIQ plan and one Major Cancer rider would mean you enjoy 2.05% p.a. on your first $10,000 for the first year.

GIGANTIQ: Deposit and withdrawals

Similar to Dash EasyEarn, there is no lock-in period for your deposits and withdrawals. GIGANTIQ also has less restrictions compared to Dash EasyEarn. For one, the minimum to get started is $50 and you only need to maintain an average daily value of $50 in the account.

Thereafter, your subsequent top-ups and withdrawals can be any amount. It doesn’t need to be in blocks of $100 or $500 unlike Dash EasyEarn.

One minor inconvenience is that you can only make top-ups via DBS/POSB bank account, or via your Etiqa eWallet. When you withdraw, you may receive your funds via PayNow or to your own POSB or DBS account. Do note the withdrawal charges too:

- $0.50 for each withdrawal to a DBS/POSB account

- $0.70 for each withdrawal via PayNow

Dash EasyEarn or GIGANTIQ

Both Dash EasyEarn and GIGANTIQ are actually insurance plans underwritten by Etiqa. For both, you’ll be covered for up to 105% of your total account value in death benefits. However, note that the usual exclusions such as from death from suicide within the first 12 months, or death due to pre-existing conditions will apply.

Both plans are also covered under the Policy Owners’ Protection Scheme, administered by the Singapore Deposit Insurance Corporation (SDIC). The amount insured has a guaranteed surrender value capped at $100,000, so your money is safe with either option.

More importantly, the money you keep in both Dash EasyEarn and GIGANTIQ can be withdrawn easily at any time. The withdrawal fee of $0.70 is an annoyance, but not a deal-breaker.

Personally, The Frugal Fox thinks that a good strategy for your emergency funds will be to go with Dash EasyEarn to max out the 1.8% p.a. for your first $20,000.

If you have excess funds, then direct them to GIGANTIQ to get another 1.8% p.a. on your first $10,000 with them.

But what if you have $50,000 or $100,000 in spare cash? If you have maxed out the account limits for Dash EasyEarn and GIGANTIQ’s 1.8% p.a. promotional rate, but still want to earn a decently high return on the rest of your cash, cash management products may be the answer.

To find out what the fox says about the cash management products from Syfe, Endowus and Stashaway, check out our post here.