The current pullback in the Singapore REIT (S-REIT) sector is a “healthy correction” rather than the start of a prolonged downturn. With the bulk of Singapore’s economy poised to recover this year – our 2021 GDP has been forecasted at 4% to 6% – now could be time for investors to accumulate more REITs at better valuations.

Explaining the pullback

With economic recovery in sight for much of the world and a global vaccine roll-out underway, the 10-year US Treasury yield has been quietly climbing in response to stronger economic growth prospects and the possibility of higher inflation. The yield on the benchmark 10-year US Treasury note is around 1.37% at this time of writing, its highest since February 2020.

Given the close correlation in interest rate movement between US and Singapore, the yield for the Singapore 10-year bond has also risen in tandem to around 1.32%.

This rise in bond yield has weighed on investor sentiment given that S-REIT share prices typically face downward pressure when 10-year yields rise, at least in the short term.

Over a longer time period however, this trend tends to reverse. According to DBS Research, since 2013, S-REITs have outperformed the Straits Times Index (STI) in the subsequent six to 12 months after the hike in 10-year yields starts to taper off. This suggests that investors can benefit from the upside potential if they buy into the current weakness now.

Why REITs remain resilient over the long term

Despite the current pullback, S-REITs are still a fundamentally resilient asset class. Firstly, the value of REITs is well-anchored by physical real estate, which in land scarce Singapore, trends upwards over the long term.

Secondly, REIT rental income tends to be stable, due to the lock-in nature of leases. This allows REITs to pay out dividends on a sustained basis, albeit at reduced levels in certain situations, as we saw during the COVID-19 pandemic.

Lastly, there is strong regulatory support for S-REITs given their significant representation in the Singapore market. S-REITs make up over 25% of SGX’s daily turnover and about 12% of Singapore’s overall listed stocks by market capitalisation.

Some of the new regulatory measures announced in April 2020 include increasing S-REITs’ leverage limit from 45% to 50%, and extending the timeline for them to distribute at least 90% of their taxable income from three months to 12 months to qualify for tax transparency.

S-REIT yields still look attractive

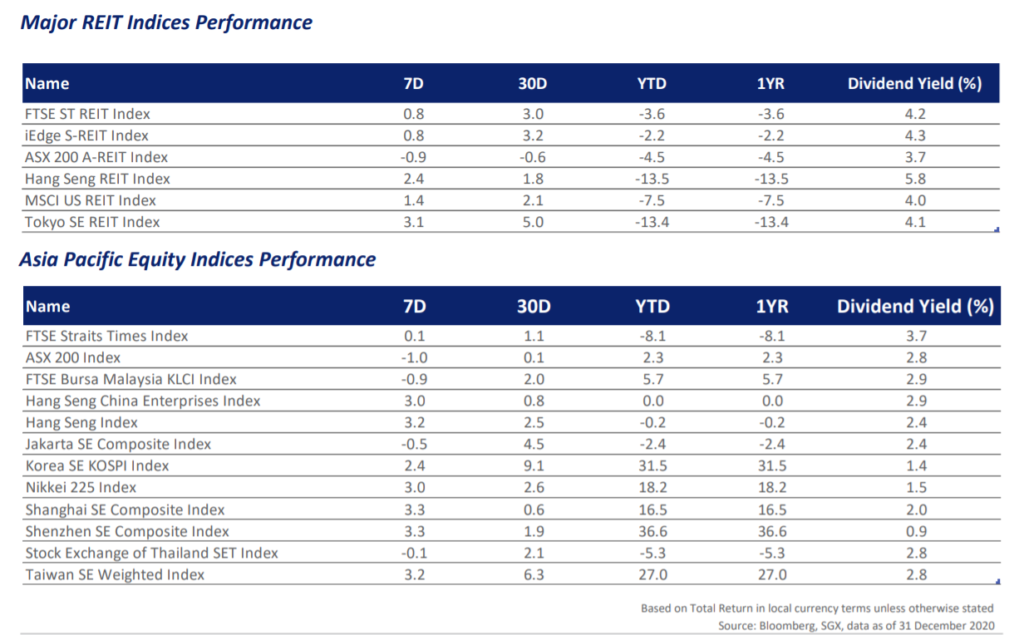

Historically, the Singapore REIT sector has averaged a 6% to 7% dividend yield, although the yield dipped to 4.3% (as of 31 December 2020) as S-REITs grappled with the COVID-19 pandemic.

While 4.3% represents a lower-than-average yield for Singapore REITs, it is still one of the highest REIT yields globally. The yield also outperforms that of other equity indices in the APAC region. Ultimately, S-REITs still provide attractive yields in the current low interest rate environment. (For comparison, the 10-year Singapore bond yield is a paltry 1.3%.)

Moreover, it is likely that we will see a distribution per unit (DPU) recovery for many S-REITs in 2021, in line with Singapore’s broader economic recovery. For one, although many REITs retained cash to disburse to their tenants as rental rebates in 2020, these sums ultimately have to be paid out at a later date this year. As we noted earlier, S-REITs are required to distribute at least 90% of their taxable income to qualify for tax exemption.

Business conditions have also improved for several sectors such as industrial and retail REITs. Rising e-commerce demand and supply chain diversification continue to bode well for industrial REIT names in 2021 while shopper traffic and retail sales have picked up with Singapore’s re-opening. These positive factors should spur DPU growth this year.

Keeping a long-term perspective

Despite the headwinds we have seen in recent weeks, S-REITs have the potential to grow further once the 10-year bond yield stabilises and the vaccine-led recovery begins in earnest.

Investors should capitalise on the current opportunity to ride this growth for the medium to long term. One way is to adopt a dollar-cost averaging (DCA) strategy where you can accumulate more REIT holdings at lower prices during market dips.

This ensures you don’t miss out on the best days that make up some of the market’s strongest performance. These best days are impossible to predict, which is also why time in the market is more important than timing the market.

If you have been adopting a DCA strategy, abandoning it now is probably not a good idea, even if it feels “safer”. With S-REITs on the uptrend for the past months, your DCA strategy would have meant that you were buying fewer REIT units at higher prices.

Now that prices have corrected, buying the dip would mean you get to lower your average investment price, thereby providing the potential for higher capital gains.

This article is a guest contribution from Syfe.

The Frugal Fox says: If you’re keen to invest in Syfe REIT+, enjoy 6 months of free investing when you use our referral code SRP732ACX

You will get SGD $30,000 managed FREE for 6 months. This works out to $75 saved in fees if you invest $30,000, so don’t forget to use it if you’re signing up.