If you had bought Singtel stock nearly 15 years ago back in September 2005 and held it till today, you would have earned almost zero in capital gains. At $2.40 at this time of writing, Singtel’s stock price is at its cheapest in more than a decade.

This could be an attractive entry point for new investors. But for people who bought Singtel shares earlier on, the last 5 years has been a disappointing slide towards the dreaded $2 level. Is it time to cut loss on your Singtel stock?

Before you hit the sell button, let’s take a closer look at Singtel’s business fundamentals and whether there is any growth potential remaining for Singapore’s biggest telco.

The fragility of Singtel’s core business

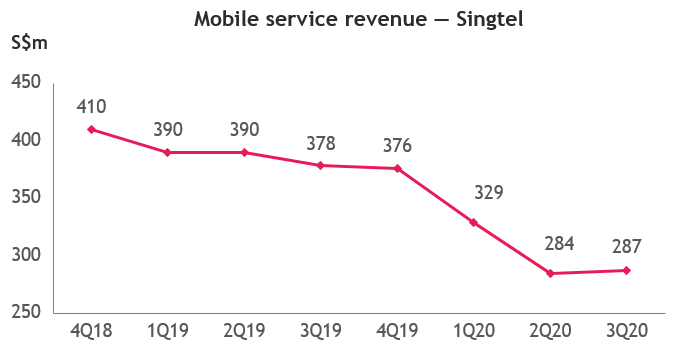

Putting aside Singtel’s dividend potential, its stock price has been on a persistent downward trend largely due to the company’s weak earnings performance. Year on year, the stock is down 29% because of the bearishness surrounding its core business and dividend cuts.

Singtel’s 9M20 underlying profit from Singapore fell 38% to S$396m and that is despite receiving S$23m income from the Job Support Scheme.

While Singtel’s consumer business was negatively affected due to COVID-19-related travel restrictions and deferment of enterprise projects, Optus (Singtel’s fully owned Australian subsidiary) fared much worse. Optus barely entered positive territory with a profit of only S$13m in 9M20 compared to a profit of S$459m in 9M19. This was mostly due to structural weakness in its Australia fixed-line business amid migration to National Broadband Network (NBN), coupled with lower equipment sales and COVID-induced weakness.

Singtel’s associates Telkomsel and Globe were heavily hit by Covid-19

Telkomsel is Singtel’s biggest associate and in FY20 contributed approximately 67% of Singtel’s total associate pre-tax contributions. (Associates of Singtel are telco companies in which they have a less than 50% stake.)

With Singtel being highly reliant on associate revenue, this is a concern. Telkomsel continues to cede market share to XL Axiata, Indosat and other smaller telco players in Indonesia. According to a DBS analyst report, Telkomsel’s overall revenue contribution to Singtel is expected to drop to only 40% in FY22 due to weak cellular business and revenue market share losses.

Globe is another Singtel associate in the Philippines. Like its competitors in the Philippines’ telco market, Globe was badly hit by COVID-19 movement restrictions.

Globe’s mobile customer base is now down 20% year on year, and has fallen 12% since March 2020. This was mainly due to the decline in acquisitions in light of the pandemic. The silver lining for Globe is that the commercial launch of a third telco in the Philippines is likely to be delayed till after the second half of 2021.

The latest entrant, Dito Telecommunity, received its telco licence in July 2019 and had been planning to launch last year.

Potential upside: Grab-Singtel digital banking license

It’s worth noting that at Singtel’s current low valuations, the market is ascribing almost zero value to the company’s core businesses.

But the company is cultivating new key businesses for the future.

In December last year, the Monetary Authority of Singapore (MAS) announced 4 successful digital banking applicants, including the Grab-Singtel consortium. Operations are expected to commence by early 2022.

This could be the start of something exciting. Singtel holds 40% of the digital bank JV with Grab. Products to be offered through this new digital bank are likely to seamlessly integrate with the daily lives of Grab and Singtel’s large, digital-first customer base.

Singtel has a subscriber base of 4.3 million (as of June 2020) while Grab has over 187 million users across Southeast Asia.

Grab’s major advantage is the customer data it has acquired through its ride-hailing platform. Grab enjoys an 80% market share in Singapore’s ride-hailing sector. It has also extended beyond its core business of ride-hailing to digital financial services, food delivery and retail.

Grab launched GrabPay wallet in 2016 and incorporated the Grab Financial Group in 2018 to provide payment, lending and insurance solutions. This experience should help Grab better understand the requirements of the underbanked segments in Singapore.

Singtel itself is a Temasek-linked entity and a trusted telecom player. This trust will enable the new Grab-Singtel digital bank to build trust among its customers to take bank deposits. Singtel is also investing in areas such as cyber security which could add value to the digital banking arm.

The Grab-Singtel consortium could very well break even in 4-5 years. The question however is whether Singtel can pivot to provide digital financial services outside Singapore.

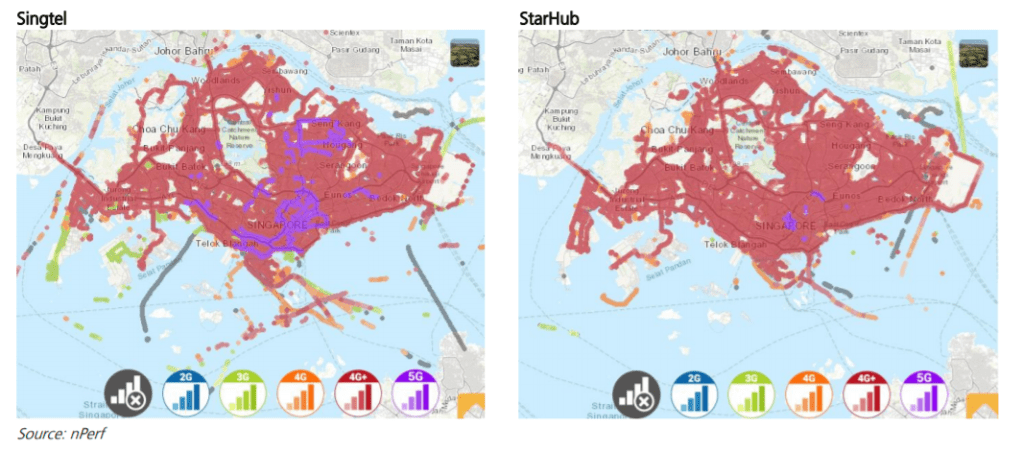

Singtel’s rapidly expanding 5G presence

Singtel has had a head start in deploying its 5G network. As the image below shows, it has outpaced Starhub in laying down its 5G network.

Singapore’s 5G networks are currently being built by Singtel and a joint venture between StarHub and M1. On 8 October 2020, Singtel launched Singapore’s first 5G standalone trial network for enterprises. The network, which utilises 3.5GHz spectrum and Massive MIMO (multiple-input multiple-output) technology, provides enterprises with early access to 5G to develop and trial run 5G solutions.

What does the fox think?

The Frugal Fox bought Singtel shares back when the stock price was at $3.80. We invested around $10,000 at that time, so we’re making a loss of around $3,683 at the current share price of $2.40.

However, we’ve also received several years of generous dividends. Our average dividend yield over the past 5 years is 6.96%. This means that we have collected about $690 in dividends each year, or $3,450 in all for the past five years.

Overall, our net loss is only around $200.

Personally, we’ve chosen to hold on to Singtel stock. As the COVID vaccine gets rolled out worldwide, we think the stock price will rise in the immediate term. We’re optimistic that Singtel’s stake in the new digital bank and its rapidly expanding 5G presence will position it well for the future too.

For us, Singtel is ultimately a dividend play. We have no illusions that the stock price will suddenly rise and hit $5. For that sort of growth, we have our exposure to US tech stocks to count on. Instead, our plan is to continue collecting dividends from Singtel.

If you do not need to raise cash right now, The Frugal Fox thinks Singtel stock could still be worth holding for its long-term dividend potential. However, if you’re looking for a faster growing stock, then you may want to evaluate whether Singtel still fits the bill for you.

Disclaimer: The information contained herein is the writer’s personal opinion on his blog and does not constitute investment advice. Please do your own due diligence before making any decisions.