Want to earn guaranteed returns of 3.21% per year? Look no further than the November 2022 Singapore Savings Bond (SSB) issue – SBNOV22 GX22110A.

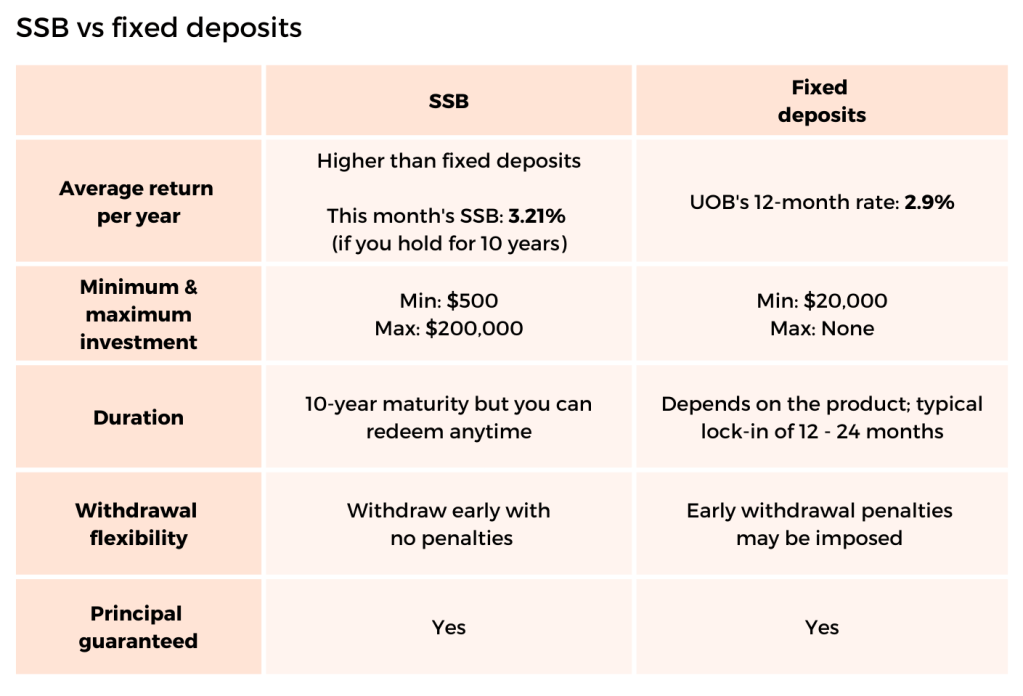

Assuming you hold your SSB for the full 10 years, you’d be getting average returns of 3.21% per year. That means if you invest $10,000, you’ll get $321 in yearly interest! Even if you just park your money there for one year, you can still earn 3.08%.

This is higher than UOB’s latest 2.9% rate for their 12-month fixed deposit. And higher than the August 2022 SSB tranche which offered a record 3% in average 10-year return.

How to apply for the Singapore Savings Bond (SSB)

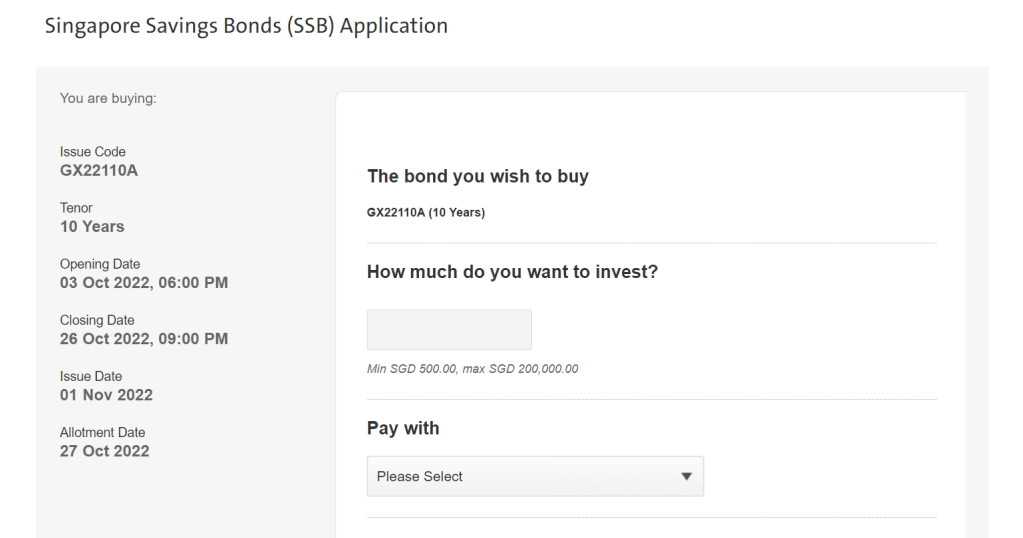

You can start applying for the SSB from now to 26 October, 9pm. The process is easy and you can invest with a minimum of $500.

Step 1: Log in to your internet banking (DBS/POSB, OCBC or UOB)

Step 2: Under “Investments”, look for “Singapore Government Securities” > Singapore Savings Bonds (SSB).

Step 3: Click buy. Remember to have your CDP account number with you.

P.S. Take note that you can only buy SSBs from Monday to Saturday, 7am to 9pm

Step 4: Enter your desired investment amount. This amount will be deducted from your bank account automatically.

There’s also a $2 transaction fee for each SSB application made.

How to check your SSB allotment?

The application results will be released on MAS’ website at 3pm on 27 October 2022.

SSB will be issued on 1 November 2022 by end day. You can check your CDP account online to see your SSB holdings. Your bank will probably SMS or email you to give an update as well.

Many people will probably be applying for the November 2022 SSB issue, so you may not get the full amount that you applied for. However, you’ll get refunded for any partial application and you can try again when the December SSB application opens.

E.g. the August 2022 issue was oversubscribed and most people would have only received an allotment of $9,000. If you had applied for $20,000 of Singapore Savings Bonds, the excess $11,000 would be refunded to the bank account you used to apply.

When will you get your SSB interest?

Your SSB interest will be paid out every 6 months. Interest payments will automatically be credited to the bank account linked to your CDP account.

In other words, you’ll get your first interest payment on 1 May 2023 and the second one on 1 November 2023.

How to redeem your SSB?

One thing we like about SSB is the liquidity. You can redeem your SSB i.e. withdraw your money, at any time, and with no penalty for exiting early. This is unlike fixed deposits where you may be charged an early withdrawal penalty.

For SSB, just submit a redemption request through your internet banking (DBS/POSB, OCBC, UOB). You’ll have to redeem in multiples of $500 and there will be a $2 bank fee for each redemption.

You will then receive the full amount you requested, along with any accrued interest, by the 2nd business day of the following month. E.g. if you make a redemption in March, you’ll receive your money in April.

Should you put your money in SSB?

In these uncertain times, the stability and guaranteed returns that Singapore Savings Bonds provide can be very reassuring. For us, it’s a more flexible and attractive place to park our spare cash compared to fixed deposits.

We’ll be applying for this month’s SSB issue and subsequent issues if the 10-year average returns continue to be above 3.2%.

Final thoughts

The one drawback is that you may not get your full SSB allotment if the tranche is oversubscribed. That can be quite annoying as your money won’t be put to work efficiently.

One workaround is to keep the cash outside your SSB allotment in something more liquid like cash management accounts. Say you applied for $20,000 of SSB but only got allotted $10,000. You can put the extra $10,000 in a cash management account first while you wait to apply for the next attractive SSB or T-bill tranche.

For one, you’ll likely get a better return than regular bank savings accounts (2.1% to 4.1% p.a., depending on which product you choose). The liquidity is also pretty good which means you can get your withdrawn proceeds in a matter of days.

Are you going to apply for the month’s SSB? Where else are you parking your spare cash? Let us know in the comments!